Get Busy Living or Get Busy Dying

Hi Budgeter

Is this the end or the start of your financial journey? What else can you be doing to improve your financial situation? What can go wrong and can you protect yourself? What should you do with your savings in the long term?

A savings plan is vital, and if you have clear goals, linked them to your savings and set up the right structures than half the battle is won.

But here is the problem. A quality savings plan might allow you to achieve some smaller lifestyle goals and pay down debt, but it is a false summit. You are only half way up the mountain. To be really in control financially, you need to tackle these three things:

- Larger goals like a house upgrade

- Funding retirement

- Managing what can go wrong

These things need more than a budget and can only be partially addressed in an e-mail, but let me give you a brief rundown of what you are facing.

Larger goals like a house upgrade

Here are a few rules-of-thumb:

- Don’t believe a bank when their computers tells you that you can afford to take on more debt. You need to run a cash flow scenario with and without the large goal and project your cash flow surplus.

- You need to find a way to balance your goals and your retirement result. If you knew that getting that really nice car was going to leave you poor in retirement, would you do it?

- Don’t say “she’ll be right”. Most people retire predominately on the age pension, far from alright.

Funding retirement

This is of course, general advice, and you should only take specific actions after considering your personal circumstances and ideally receiving personal advice

Research from the Financial Services Institute of Australia suggests that if you want to guarantee your money and lifestyle lasts 30 years in retirement, the maximum you can draw from your portfolio/superannuation each year is 3.19%!

That means, at a minimum, a couple needs $1,842,759 to guarantee a comfortable retirement lifestyle (as defined by ASFA). With anything less, if you have a balanced investment profile, there is a risk of running out of money.

Taking into account inflation, that figure will likely be $2,476,513 in 10 years time, $3,328,227 in 20 years time and $4,472,589 in 30 years time.

That’s a lot of money and is probably not going to happen by accident.

You need to know how shares, property, bonds, term deposits and cash works. You need to know which of these you currently have and should have as your investments (including superannuation).

One key difference is risk. Although, at a minimum, you have to weigh up two different risks.

- Market Risk: The uncertainty of the value of an asset when the time comes to sell it. This is called market risk. This risk can be managed with investing for the long term (through ups and downs), diversification and regular investing over time.

- Longevity risk: The chance that you will not have enough money to fund a comfortable retirement (or what you do have will run out early). Half of Australians end up predominately on the age pension*, and may have underestimated this risk. Please don’t fall into this group. This risk can be managed with investments that have a high market risk, as they tend to grow in value over time.

* ABS - Retirement and Retirement Intentions, Australia, July 2012

So pick your poison? Which risk do you prefer to take on? The ups and downs, mainly over the short and medium term, or the risk of not having enough for a dignified and comfortable retirement.

If you just have superannuation building for retirement, you should at least review which type of risk you are taking on. It can make a big difference come retirement.

Don’t wait until your home loan is paid off to look at this. Time is one of your most valuable assets.

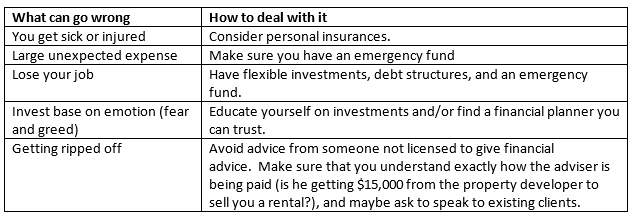

Managing what can go wrong

I cannot cover off on all things that I have seen go wrong for people financially and how those issues were addressed, as some were very specific to their circumstance. I can however, tell you about the most common:

And with that, we have made it to the end of module 6. You have hopefully escaped from metaphorical prison of earning everything you spend. Writing this, I am reminded of the end of the Shawshank Redemption:

“Dear Red, if you're reading this, you've gotten out. And if you've come this far, maybe you're willing to come a little further.”

With similar sentiments, I would like to offer you complimentary strategy session. This is where we can sit down and talk about your challenges you face and the various strategies that you might be able to look at. This meeting, like everything we do, has a focus on education. The reason I offer this meeting at no charge is that it gives us the opportunity to meet and gauge if it is worth exploring a longer term financial planning relationship.

If you would like to take me up on this offer, visit www.gpafinancial.com.au/strategysession or call 07 3170 6213

But for now, good luck on your financial journey.

Matt Boxer AFP®, BBus, Adv DipFS(FP), DipFMBM

Director/Owner

Authorised Representative | GPA Financial Planning Pty Ltd

Comments and Feedback

[fbcomments url="https://www.gpafinancial.com.au/education/budgeting-toolbox/bec-module-six/" width="100%" count="off" num="3" title ="" countmsg="wonderful comments!"]