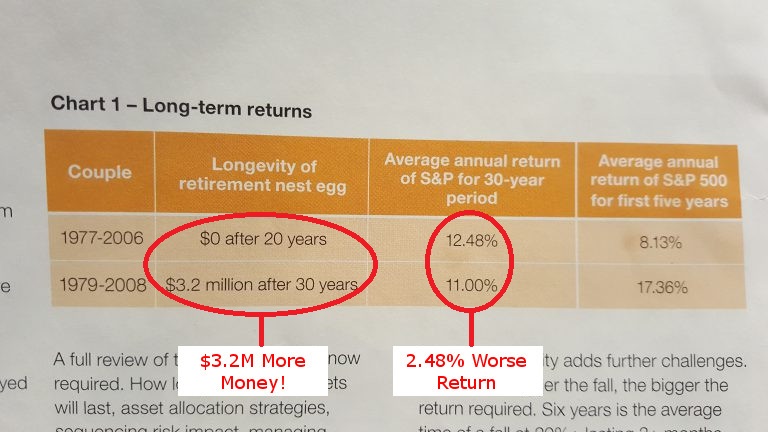

This table was taken from Financial Planning Magazine (volume 29 issue 5). To paraphrase it, someone starting retirement in 1977 runs out of money in 20 years. The same person retiring 2 years later with the same retirement capital and investment allocation, has massively different results. They still have $3,200,000 after 30 years!

This is called Sequencing Risk. It is why so many retirees needed to return to work after the GFC - BUT there are strategies you can employ to manage it.

Another telling Graph is:

If you want to read up further about Sequencing Risk, then Challenger has a good article regarding it:

http://www.challenger.com.au/about/Sequencing.asp

Sequencing Risk can generally be managed by a strong financial strategy that may include:

- Asset Allocation, including a short to mid-term spending bucket (sometimes called cushion or buffer).

- Planning around what actions should be taken if when we have another GFC type correction.

- Regular re-balancing

- A quality trusted financial planner to give you confidence not to listen to fear and implement the right strategy at the right time.

If you would like to discuss your investment strategy with GPA Financial Planning then please don't hesitate to book a free initial consultation.

Article by Matt Boxer - GPA Financial Planning

Stay up-to-date with any future news and articles

Simply sign up to our Newsletter or like our facebook page to receive:

Schedule a Free Strategy Session

A two hour discussion on your options for achieving your goals

< Back To GPA Financial Planning's Education Centre